Disclosure: This post may contain affiliate links. We may earn a commission if you sign up through our links, at no extra cost to you.

Introduction

If you’re looking for the best high-interest savings accounts in Canada 2025, you already know how fast interest rates shifted over the last two years. A good HISA can literally make the difference between letting your money sit still and having it grow automatically.

The problem? Most banks advertise “high-interest” but pay almost nothing. We tested the real rates and ranked the accounts Canadians use for emergency funds and short-term goals.

Most Canadians still leave their cash at big banks earning 0.01%, which is basically nothing. If you want your money working for you, even while you sleep, a high-interest savings account is the easiest win.

Related reading: Best Investing Apps in Canada

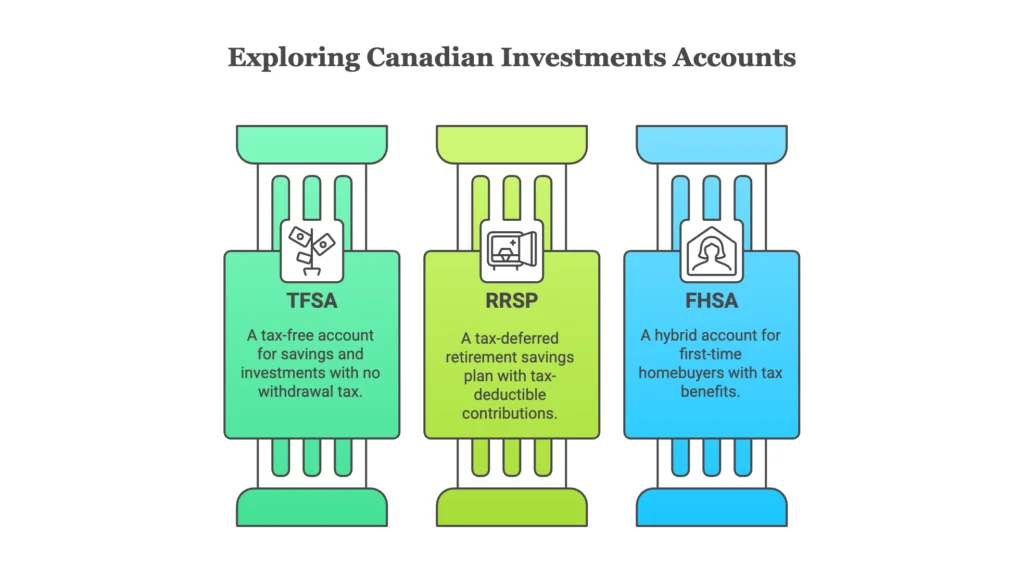

Related reading: TFSA vs RRSP vs FHSA

What Is a High-Interest Savings Account?

A high-interest savings account is a simple place to keep your cash safe, liquid, and earning a better rate than traditional bank savings accounts.

Most Canadians use HISAs for:

- emergency funds

- short-term savings

- saving for a big purchase

- holding cash before investing

And yes, online banks usually pay 5 to 20 times more interest than the Big Five.

Best High-Interest Savings Accounts in Canada (2025)

Below are the top options right now, based on rates, features, reliability, and my own experience trying almost all of these.

🥇 EQ Bank Savings Plus Account — Best Overall

Typical rate: 2.50–4.00%

Fee: $0

CDIC: Yes

EQ Bank is one of the strongest options for Canadians who want effortless savings growth. It consistently offers among the highest rates in the country, and deposits are protected by CDIC.

Why I like it: It’s simple, fast, and their app never causes headaches. EQ’s customer service is also surprisingly good for an online bank.

Learn more: https://www.eqbank.ca/

🥈 Tangerine Savings Account — Best for Welcome Bonuses

Base rate: 0.70–1.00% (promos up to 5%)

Fee: $0

CDIC: Yes

Tangerine’s promotional rates are the real attraction. If you’re new to the bank, you can often earn 4–5% for the first few months.

Insight: If you’re switching banks or opening a new account anyway, claiming a bonus here is an easy extra win.

Learn more: https://www.tangerine.ca/

🥉 Wealthsimple Cash — Best for Spending + Saving

Rate: 2.00–4.00% depending on membership

Fee: $0

CDIC: Yes

This hybrid account lets you save, spend, and invest in one place. Fast transfers, clean interface, and perfect for people who want simplicity.

Tip: If you’re already investing with Wealthsimple, keeping your cash here keeps everything under one roof.

Learn more: https://www.wealthsimple.com/en-ca/

Simplii Financial High-Interest Savings Account — Best Big-Bank Alternative

Rate: 1%–3%

Fee: $0

CDIC: Yes

Backed by CIBC, Simplii is familiar, reliable, and still offers decent promotional rates for new customers.

Learn more: https://www.simplii.com/en/index.html

Neo Money Account — Best App Experience

Rate: 2.25–4.00%

Fee: $0

CDIC: Yes (through partner bank)

Neo offers one of the cleanest modern banking apps in Canada. Great for people who care about user experience and fast movement.

Learn more: https://www.neofinancial.com/

HISA Rate Comparison (2025)

| Bank | Rate | Fees | CDIC | Best For |

|---|---|---|---|---|

| EQ Bank | 2.5–4.0% | $0 | Yes | Best overall |

| Tangerine | 1–5% | $0 | Yes | Bonuses |

| Wealthsimple Cash | 2–4% | $0 | Yes | Spending + saving |

| Simplii | 1–3% | $0 | Yes | Big-bank alternative |

| Neo | 2.25–4% | $0 | Yes | App experience |

Should You Put Your Emergency Fund in a HISA?

Short answer: yes.

Your emergency fund should be:

- safe

- easy to access

- not exposed to market risk

A HISA checks all these boxes.

Related reading: How to Build Wealth in Your 20s

HISA vs TFSA vs GICs — What’s Better in 2025?

- HISA → short-term money, flexible

- GIC → higher fixed rates, but locked

- TFSA → long-term investing power, tax-free

Related reading: TFSA vs RRSP vs FHSA

{kind=link}

If you’re building wealth in your 20s or 30s, think of HISAs as the waiting room for your real investments, not the final destination.

How Much Should You Keep in a HISA?

Most Canadians should aim for 3–6 months of living expenses.

A quick breakdown:

- in your 20s: $3,000–$12,000

- in your 30s: $6,000–$25,000 depending on kids, rent, and debt

Everything extra should usually go toward investing.

Personal note: “I once left nearly $20,000 sitting in a 0.01% account for a whole year… I still cringe thinking about how much growth I missed.”

Common Mistakes to Avoid

❌ Leaving cash at big banks earning nothing

❌ Keeping too much money in cash

❌ Missing welcome bonus promotions

❌ Not using TFSA for investing

Small changes here literally add up to thousands over a few years.

FAQ — High-Interest Savings Accounts in Canada (2025)

1. Are HISAs safe in Canada?

Yes. As long as the institution is CDIC-insured, your deposits are protected up to $100,000 per category.

2. Are online banks trustworthy?

Absolutely. EQ Bank, Tangerine, and Simplii have been trusted for years and are regulated just like traditional banks.

3. Can I lose money in a HISA?

No, HISAs do not fluctuate like stocks or ETFs.

4. Do promotional rates matter?

Yes. If you rotate banks once a year, you can keep earning 4–5% consistently.

5. Should I use a HISA inside a TFSA?

Only for temporary savings. Long-term TFSA money should be invested.

Final Thoughts

Choosing the best high-interest savings accounts in Canada 2025 is one of the easiest financial wins you can take today. Your money stays safe, grows automatically, and stays ready for investing when you’re ready.

Start with one account, automate deposits, and let your savings build momentum.

Related reading: Best Online Brokers Canada

Related reading: Best ETFs for Canadian Investors